Behind every stock | June 2025 Update

"Behind every stock is a company. Find out what it's doing." - Peter Lynch

Image generated by Grok

THE MONTH | June has historically been a seasonal low but the Fund bucked the trend this time to end FY2025 with a 6.4% gain (v. -0.5% for the S&P/ASX Emerging Companies Index), driven by a re-rating of defence-focused cybersecurity play Archtis (AR9) and modular data centre company DXN (DXN).

THE QUARTER | AR9’s strong end to FY25 was a key factor in the Fund’s quarterly return of +8.5%. A valuation catalyst for an unlisted investment was another key move. Tech-oriented nanocaps countered some of the gains, likely influenced by tax loss selling in May and June.

FY2025 | The Fund started and ended FY2025 with strong quarters but struggled in between, leaving it down 3.7% at June 30. Tech sector exposures were both the strongest and weakest contributors. Digital ad fraud detection software developer Adveritas (AR9) and an unlisted investment led the way. MedTech company MedAdvisor (MDR) and remote monitoring tech co Spectur (SP3) were most responsible for the negative net outcome.

SMALL TALK | Fund investors can access our weekly Small Talk updates, in which we have profiled Dataworks (DWG) and MDR since the previous monthly fund update.

OUTLOOK

The major themes dominating equity markets for the past three years - themes that have not been supportive for smaller stocks - remain intact entering FY2026. We see them as the feedback loop created by the rise of index investing and the excitement around "Artificial Intelligence” (AI).

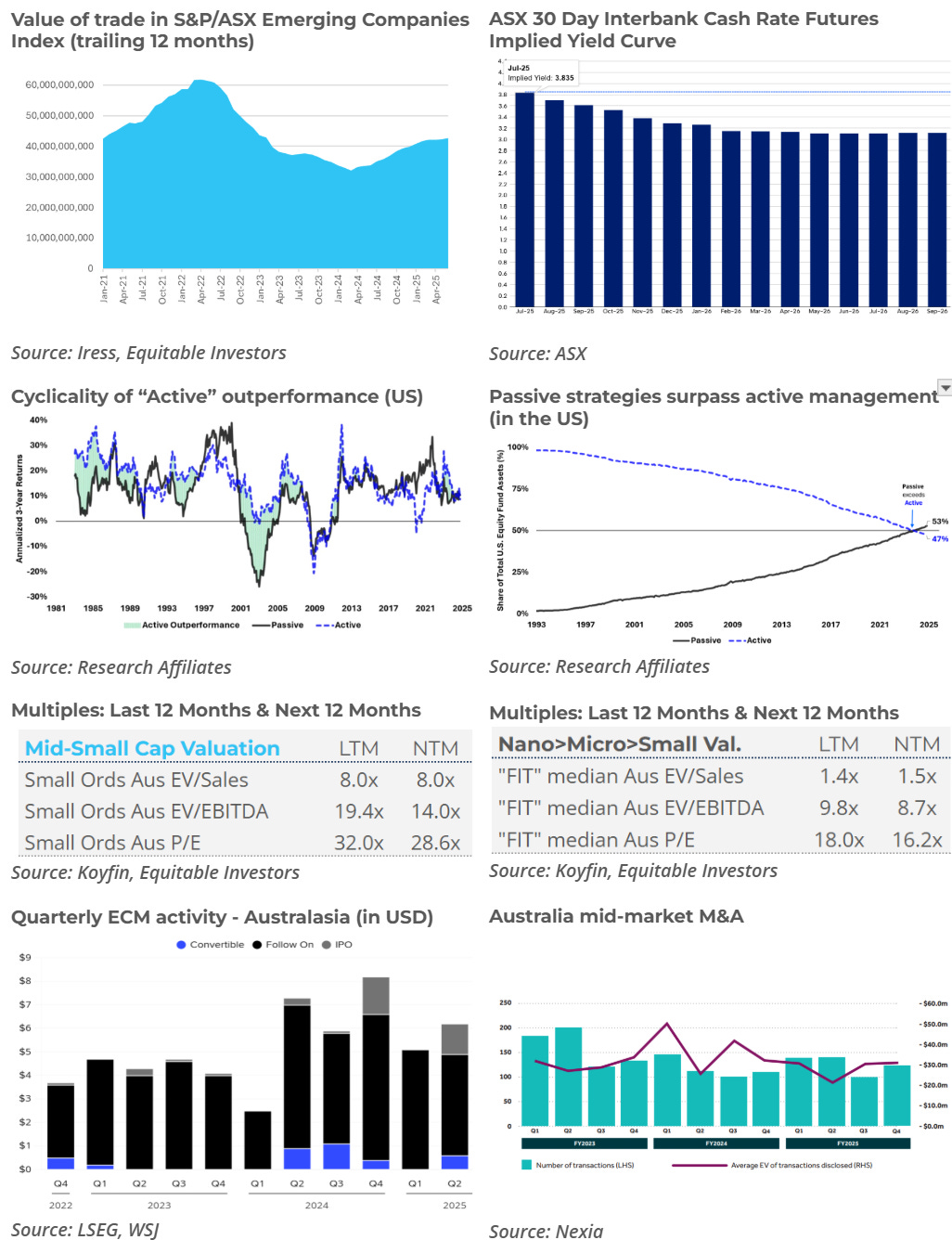

But there have been subtle shifts in the behaviour of market participants that appear to be more supportive of smaller stocks. Quantitatively, we have seen trading activity in the S&P/ASX Emerging Companies Index lift above multi-year low. Empirically, we have observed investor interest being recaptured by select microcaps with good stories to tell. At the macro level, the scene is set for modest interest rate cuts in Australia and the US as long as inflation remains under control.

It has been a hard grind for the past three years. Our expectation is that many of the companies Dragonfly Fund is invested in are getting closer to valuation catalysts. Strategy execution and demonstrating self-sustainability are key. For some companies the valuation catalyst may be via acquisition. In a bifurcated world where index inclusion puts a stock in a different valuation class to those outside major indices, there is a nice valuation arbitrage and supplement to earnings growth available for index-included trade buyers.

Geopolitical volatility continues to generate plenty of noise in markets, with no indication that a period of calm lies ahead (the war in the Ukraine continuing on, hostilities continuing in the Middle East and international ties being tested by US President Trump). But commercial activity continues on and opportunities continue to emerge. Smaller companies are generally better placed to nimbly navigate their way around markets.

In such an environment, we would rather be invested in a small but ambitious business on a low valuation than a bloated bank priced at nearly 30x forecast EPS but expected to grow earnings <3% a year. On the flipside, the feedback loop referenced above means that, until a structural shift is triggered, in the words of Research Affiliates, “passive inflows perpetuate price trends… and capital shifts further into passive strategies”.

At some point in the future, after some trigger (unknown to us today) leads to a structural shift in markets, we can envisage an official government enquiry into why Australia’s major superannuation funds continued to pour their capital into stocks that were over-priced on almost any valuation measure. It is going to be interesting to see how things pan out for Australian Super after it decided to go underweight CBA (~12% of the S&P/ASX 200 index) on fundamentals. Other super funds have maintained index weightings in CBA on fears that fundamentally-driven investment decisions to stray from the index may lead to underperformance if “passive” flows continue to drive demand for CBA, in turn leading to regulator APRA placing restrictions on them for failing the performance test in two consecutive years.

We are confident Peter Lynch’s reminder that “behind every stock is a company” will become relevant again.

MONTHLY PORTFOLIO REVIEW

Briefly, in June cybersecurity company Archtis (AR9) was awarded a contract by a prime government contractor for the US Department of Defence, then added a contract with a UK defence contractor. AR9 then proceeded to raise $7.5m. Late in the financial year modular data centre maker DXN (DXN) announced a series of new contracts, including two in June worth $6.2m. The weakest performers in the portfolio, IMB and DWG, suffered from an absence of news rather than any actionable event occurring.

CHARTS

WHAT’S ON OUR MINDS

Price Discovery

Index-tracking; momentum and quantitative strategies have caused a structural shift in equity markets and the allocation of capital no longer seems to occur across a broad cross-range of companies. In the words of Research Affiliates, “passive inflows perpetuate price trends… and capital shifts further into passive strategies”.

M&A

Global M&A is up 31% year-on-year in US dollar value for CY2025-to-date (as of July 15, 2025) and in Australasia the aggregate deal value is up 78%, lifted up by the bid for Santos (STO). There has continued to be a regular flow of transactions involving small-to-mid cap ASX-listed companies.

Liquidity

Trading in the S&P/ASX Emerging Companies Index has remained well below the peak dollar values of 2022 (31% below the peak 12 month period, which ended April 2022) but up 26% year-on-year, using the 12 month trailing trade value in the Emerging Companies Index (through to the end of June 2025) as a proxy for micro and small caps.

Private market valuations

Private markets continue to slowly adjust to changes in the cost of capital that have occurred over the past few years. Despite marketeers labelling private assets as low volatility, there is underlying volatility in the pricing of private assets AND correlation with public markets.

Private equity funds claim volatility of ~10% but private equity funds listed in the UK have exhibited 24% volatility and are priced at a 30% discount to NAV, noted Verdad Capital.

“Every VC-Backed IPO in the Past 12 Months Has Been a Down Round” declared The Information in May.

Asian private equity assets are trading at 30-40% discounts according to Bloomberg.

In US secondary markets for VC-backed companies, on average, the ZX Index Values for June 2025 sat at a 5.2% premium on the last round price per share, while the average bid-ask spread was 7%.

Our private Investments

A key lesson for us when investing in unlisted entities has been the importance of having adequate influence with the investee. When problems arise, exiting private investments is often not an option. But if we can influence the actions taken in response, we can push for the best possible outcome.

“Recap” risk and opportunity

We analysed quarterly cash flow reports for the June quarter of 2024 and found over 262 companies with no more than four quarters of cash funding at hand based on their most recent burn rates - and also 95 companies in net debt positions that reported negative operating cash flow. With these companies competing for new capital, there is a funding risk for existing investments that are not self-funding at this stage. The situation is also an opportunity for investors to apply bottom-up, fundamental research and provide attractive companies with capital on attractive terms.

Interest rates & inflation

Interest rates remain low by historical standards (see 700 years of declining rates charted here). We are entering FY2026 with modest expectations in markets for official interest rate declines in both Australia and the US. Rate cuts are typically positive for equities - and small caps in particular - BUT large cap equities traded strongly through the last rate hiking cycle and equity risk premiums currently appear low, especially for larger cap equities.

Energy

The world is going to need all forms of energy to sustain or further advance standards of living. “Electricity demands from AI data centres are outstripping the available power supply in many parts of the world” already, reported Bloomberg. Dragonfly Fund does not invest in the resources sector directly but we do seek opportunities to participate in the energy economy.

Applications to invest in Equitable Investors Dragonfly Fund can be made online with Olivia123.

10k Words | July 2025

We get a bit fixated on US equity valuations, with Vanguard highlighting the high hurdles required to achieve another decade of >12% returns; even as the 10 year bond yield has been more competitive and tariffs drive negative earnings revisions in the US. The Ex-US equities world has been fairing better out of the tariff scenario. We check in on interest rate expectations in the US and Australia. Bain bemoans a softer global buyout environment lately while The Information tackles the private market liquidity problem graphically. Finally, the US office CMBS delinquency rate charts near-vertical while Aussie mortgage arrears have been on the rise.

Dragonfly Fund has the capability to "swap" shares in a company or companies for Dragonfly Fund units where Equitable Investors finds them attractive and suitable investments. If you have a stock in your bottom drawer that we might be able to do something with, please reach out. NOTE to date we have used this capability sparingly, rejecting all but a very small number of proposals, but we continue to seek favourable opportunities.

Want to catch up?

If you are interested in learning more, please get in touch via mpretty@equitableinvestors.com.au and we will be pleased to arrange a meeting.