Farewell FY2023 - June 2023 Update

"You make most of your money in a bear market. You just don’t realize it at the time. It causes you to make the tough decision of whether to hold or buy more shares” - US investor Shelby Davis

THE MONTH | On the surface, June was a month in which we watched the final rush of end-of-financial year tax loss selling, with a basket of positions all under pressure as a result. Compensating for that was the reaction to a transformational acquisition and refinancing by Intelligent Monitoring (IMB) and contract wins by Archtis (AR9), leaving the fund down 0.7% for the month. There was a lot of manoeuvring to ensure the Fund could take advantage of tax loss selling where it could - and participate in several capital raisings, all of which we believe have set things up for the new financial year.

THE FISCAL YEAR | It was a bitterly disappointing year thanks primarily to the permanent loss taken on unlisted investment Ellume, which was responsible for over half the fund’s loss for FY23 (see our September 2022 report). During the year we added a “What’s on Our Minds” column to these reports and one of the key lessons noted is that you need influence over unlisted investments. Other losing positions were not of the same scale as the strongest positive contributors, being MedAdvisor (MDR) and IMB, but there were more of the losers, in an environment where the smallest stocks on the ASX averaged a -36% return (see our “FIT” Universe review).

PORTFOLIO REVIEW

There was only a small number of investments that made notable gains in the portfolio in the month of June as most positions either treaded water or battled the final round of tax loss selling before June 30.

Security monitoring company Intelligent Monitoring (IMB) topped the list of gainers. We highlighted in the previous monthly update that IMB had been the greatest drag on the Fund in May, falling 29%, but that in June it had gone on to announce a transformational acquisition and funding restructure (see “Monthly Movers” below) that has caused its stock to rally.

As you can see from screenshots here, there were literally zero bids on the screen for IMB at times. This is a great example of the backdrop we currently see in microcaps - the market price can be completely detached from any concept of fundamental value because, as we have quoted hedge fund manager David Einhorn concluding, “Nobody is paying attention, nobody is doing the work, nobody cares what the company says. There's just nobody home”.

Against this market backdrop - where one could argue that the ASX has failed the vast majority of its corporate customers - we think you have to have a “private equity in public markets” approach and the story of IMB, with a catalyst renewing market interest in the story, is a great example.

Monthly Movers

Intelligent Monitoring (IMB; $45m market cap; +60% change in price for the month) | The security monitoring company agreed to acquire ADT’s Australian business, transforming the scale of IMB. This transaction is said to deliver pro-forma EBITDA of $24.8m for FY23, without factoring in any cost-out opportunity. IMB has agreed to pay $45m cash, with adjustments for working capital, funded by debt and a $15m rights issue. Clients can see our “Stock in Profile” summary here.

Archtis (AR9; $33m market cap; +17%) | Late in June the secure information sharing platform developer won a $4.06m contract from the Australian Department of Defence (DoD) - for software licences and services to conduct a proof of concept evaluating productivity, compliance and security gains for the Defence office environment.

MadPaws (MPA; $35m; -17%) | The online pet services business reported ~146% revenue growth to between $24.5m and $24.7m for FY23 that translates to 58-60% on a pro-forma basis (taking into account acquisitions). MPA said it is “on track for EBITDA positive in Q1”. Clients can see our “Stock in Profile” summary here.

Updater (Unlisted) | The Fund had a small residual holding in Updater after selling down its holding when Updater chose to delist from the ASX several years ago, arguing it would secure a materially larger valuation in the US. Updater announced a material “downround” in order to raise working capital for its contract servicing the US defence force - so we have written down our holding by ~95%. There are parallels here with Ellume that further reinforce our view that influence with the company is required when entering unlisted investments.

Other news flow from across the portfolio during the month (as presented each week in our Small Talk update for clients):

Adveritas (AV1; $30m market cap; -4.3% change in price for the month) | The ad fraud prevention software company said it achieved record annualised revenue of $3.9m due to new contracts and up-sells. Annualised revenue has grown over 130% since January 2022. In particular, betting companies William Hill and Superbet have been up-sold by 40% and 60% respectively.

Droneshield (DRO; $202m; -17%) | The anti-drone technology company said it received the remaining payment following successful completion of delivery of the all-time record purchase order of approximately $11m for a Government agency customer, announced on 21 December 2022. The payment timing is in line with the original timetable. The amount, approximately $5m, will be reflected in the 2Q23 receipts.

Firmus Grid (Unlisted): ST Telemedia, a leading Singapore-based data centre provider, announced a significant investment into a global venture with Firmus, a leader in highly scaled immersion cooled computing platforms. The venture will launch a GPU-centric “Infrastructure-as-a-Service” offering focused on deep learning AI and visual computing workloads, to be known as Sustainable Metal Cloud. The offering will be launched in Singapore, India and Australian in 2023. Firmus’ HyberCube technology is among the most efficient compute platforms in the world, with a sub 1.05 PUE (Power Usage Effectiveness - lower is better). Next DC claims an “industry leading PUE of 1.38.

MedAdvisor (MDR; $120m; +2%) | The MedTech company said it expected annual revenue to be up by 40%+ to between $95m and $97m for FY23. It projected EBITDA of -$3.5m to $3.0m, which is understood to be inclusive of $4.1m in one-off costs (using Peloton Capital’s numbers) for integration of the GuildLink acquisition, cloud migration and redundancies. That equates to an underlying positive EBITDA of $0.6m+. MDR said there would be $2m in cost savings from a headcount reduction following the GuildLink integration. MDR said: “MedAdvisor has positioned itself for profitability in FY24. Moreover, the Company's current US pipeline is materially above the previous corresponding period.”

Parpera (Unlisted): The financial management app developer announced its partnership with UK-based cross-border financial services firm Wise. Initially, Wise will enable Parpera to offer access to a Business Account, Business Debit Mastercard, and payments - along with Paprera’s invoicing, cash flow and tax management solutions - all in the one Parpera App. The offering will then extend to multi-currency wallets and cross-border payments. The news featured here in the AFR.

Veem (VEE; $60m; -13%) | The engineering business with marine gyroscope technology said revenue for FY23 would be ~$60m and EBITDA and profit would be “ahead of analyst forecasts of $8.3m and $2.9m respectively”. It said the Gyro business contributed $5m to FY23 sales and had $11m of orders in hand. It also announced an agreement with Strategic Marine to sell a further 12 gyros over the next three years. It also noted that it invested $5.5m in capex in 2H23. Clients can see our “Stock in Profile” summary here

Portfolio Changes and the Recap Theme

No change to our Top Nine Positions this month. Beneath the surface, we chipped away at some of the opportunities presented by tax loss selling, participated in a few capital raisings and reduced some exposures to fund all that,

There have been several changes to our Top Nine over the course of the financial year. Ellume obviously dropped out. We chose to sell down EDU Holdings (EDU) and lock in gains when its price spiked on enthusiasm for the recovery in Australia’s international student inflows. We exited financier Earlypay (EPY) after it recovered from the lows that followed news a large borrower, RevRoof, had collapsed. Our assessment was that EPY had not conducted business in this case in accordance with its representations about how it managed risk and that it was going to have to go through a period of change to ensure internal controls were functioning well (the latest change is appointment of a new CFO mid-June).

“FIT” Universe - FY23 Review

Equitable Investors is more interested in the actual performance of stocks than of market-cap weighted S&P/ASX indices that do not reflect what happens across the 2,000-odd underlying ASX listings. We track our “FIT” (Financials, Industrials & Technology) universe by measuring the share price performance of >600 companies that meet the following criteria: ASX-listed; Market caps of between $10 million and $5 billion; at least $5m annual revenue in the previous financial year; and ex- mining and energy sectors.

Here are some key data points from the financial year just ended for this “FIT” universe:

The median price change of all “FIT” stocks was -7.2%

But there was a clear size bias:

Companies with market caps <$20m averaged a -36% return

Companies with market caps in the $1 billion to $5 billion range returned an average +18%

The worst space to be in was to own <$20m market cap Consumer Staples stocks - they fell 60% on average

In terms of valuation, using EV/EBITDA, lower multiple stocks performed materially better than higher multiple stocks - but negative EBITDA stocks actually performed even better

From a momentum perspective, the “winners” from FY2022 outperformed the “losers” again in FY2023.

Online fashion retailer Cettire (CTT) was the best performed stock in the “FIT” Universe with a 640% gain, including a huge gain in the month of June, but still not enough to get it back to its 2021 peak

At the bottom of the pile was Phoslock Environmental (PET), which lost 95% after its shares were relisted in the wake of a fraud.

Cash burners featured prominently among the biggest falls for the year - they took eight spots among the worst ten.

OUTLOOK

There’s no hiding the fact that the Fund’s marked-to-market NAV has suffered a material drawdown. The Ellume experience was particularly detrimental as it represented a permanent loss of capital - and one we believe was avoidable if Ellume’s board had been less ambitious in the valuations they were pursuing (and accepted an IPO on the ASX at what we think was a reasonable valuation available to them relative to much larger figures thrown around by corporate advisors in the US).

Here is how we see things from here:

There has been a strong rebound in July (as of the day this is written), partly due to the end of tax loss selling that weighed on illiquid stocks in May and June and partly due to positive developments being recognised for specific companies.

Small and micro cap stocks with solid fundamentals and growth opportunities appear to us to be ripe for a broad re-rating after being unloved for a prolonged period. The timing of this broad re-rating is never obvious but we do believe that the recent trend of a select few mega caps generating all the market gains cannot continue and market interest in a broader range of stocks is necessary for markets to remain buoyant.

Just over a year ago we called out that it was ‘Time for Recaps” and presented the theme here - being the opportunity for investors with cash to buy into businesses at far more attractive prices in this changed environment where capital now has a real cost. Since then we have seen cash burning companies find it harder and harder to raise new capital. In the past week we have been shown an equity raising priced at a 40% discount to its 15-day VWAP and on an enterprise value of less than $2m for a company expected to generate ~$6m revenue; and we heard a capital raising pitch from a company with a much larger revenue base that was unsure what price it could raise at (and a week later has not come back with anything firm). There have been several opportunities to provide fresh capital that we found attractive and participated in over the past year and we expect there will be more.

In recent months we have begun seeing some of the catalysts and progressive evidence required to drive market repricing of our investments in a low liquidity environment where a “private equity in public markets” approach is highly relevant - as evidenced in some of the company-specific notes in this update.

When we look at our internal valuations, the upside cases are exciting. We think IMB, which has continued to make gains in July, is a good case study of sticking to valuation discipline when the listed market is clearly not functioning as a liquid and efficient price setter in the short term.

Sticking with the IMB example, the company now has a market cap of $53m and pro-forma net debt of $67m for an Enterprise Value of $120m - which is far from demanding when it is only 3.9x forecast FY24 EBITDA of $31m. If the equity doubled again from here, the multiple would remain less than 6x. The last ASX exposure was Signature Security, which was 95% owned by listed investment vehicle Oceania Capital and was sold on 11.6x reported EBIT. Back in February 2011 when that deal was announced, the RBA cash rate was 4.75% and the 10 year government bond rate was 5.5% - higher costs of capital than we currently face.

AV1, as an example from a different lens on value, currently has a $32m market cap, AV1 is not expected to be EBITDA positive until FY25 but it has cash on hand after raising $6.5m from a placement in May 2023 to add to $3m cash it held already. If you believe AV1 has a compelling solution that will continue to scale (annualised revenue has grown 130% between January 2022 and June 2023), valuation through a long-term Discounted Cash Flow (DCF) model can dwarf the current share price - broker MST’s DCF as an example uses am 18% cost of equity and spits out a valuation of $0.20 a share, 4x the current share price. We consider varying scenarios in our own valuation process and can see valuation remaining compelling with more conservative projections.

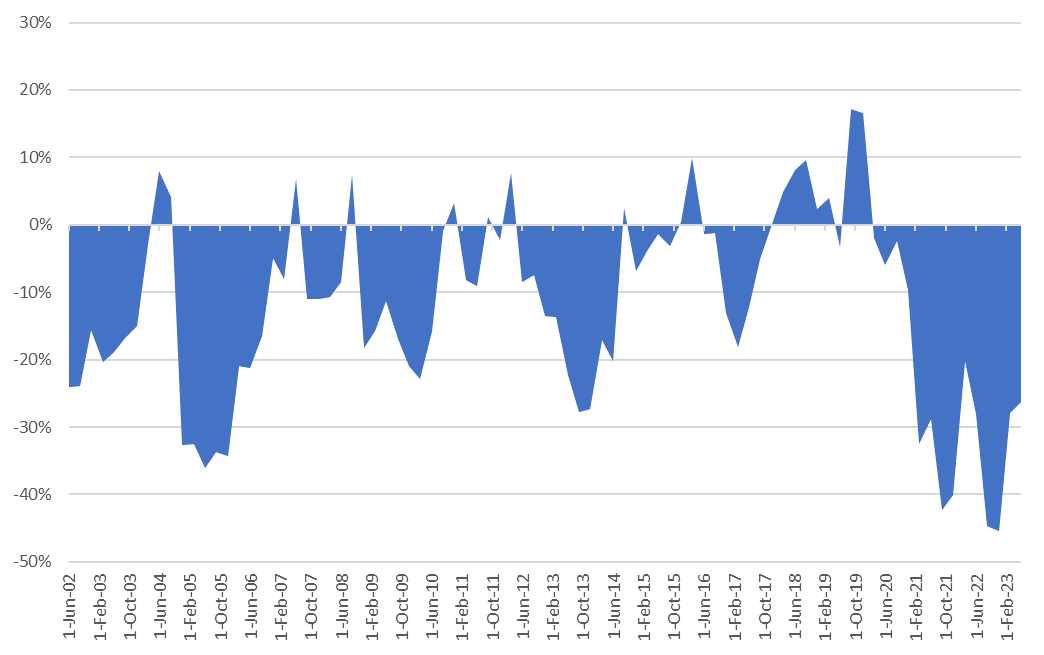

Figure 1: Discount of the S&P/ASX Small Ordinaries Index (small/mid caps) PE multiple v S&P/ASX 100 Index (large caps) PE multiple

Source: Iress, Equitable Investors

Applications to invest in Equitable Investors Dragonfly Fund can now be made online with Olivia123.

Twitter

A Pivotal Earnings Week Looms for High-Flying Stock Markets | Bloomberg

America's $1.4tn risky corporate loan market has been hit by the biggest slew of downgrades | @jessefelder

Investing in AI: Navigating the Hype | Sparkline Capital

$8CO reported an 87% increase in revenues | @DMXAsset

An early investor in AI Explains… | Bloomberg

Dragonfly Fund has the capability to "swap" shares in a company or companies for Dragonfly Fund units where Equitable Investors finds them attractive and suitable investments. If you have a stock in your bottom drawer that we might be able to do something with, please reach out. NOTE to date we have used this capability sparingly, rejecting all but a very small number of proposals, but we continue to seek favourable opportunities.

Want to catch up?

If you are interested in learning more, please get in touch via mpretty@equitableinvestors.com.au and we will be pleased to arrange a meeting.